3.3 Using Government Financial Statistics to Construct NTA

Introduction

Government Financial Statistics maintained by the IMF and the UN System of National Accounts draw on the same data and are harmonized, but they rely on different classification schemes and there are some important differences that need to be understood. Each offers their advantage and disadvantage and in some cases researchers may not have access to both sources of information.

An important point is that the SNA provides a complete system of accounts that encompass both the public and the private sector. Given that NTA encompasses both the private and public sectors of the economy, the SNA provides a comprehensive and consistent framework for the development and construction of NTA.

Public Transfers

Public transfer outflows in NTA consist primarily, but not exclusively of Revenue classified into four broad categories in GFS:

- Taxes

- Social contributions

- Grants

- Other revenue

Taxes are defined in essentially identical ways in GFS and SNA. An important distinction is drawn between direct taxes and taxes on products and production (indirect taxes) in SNA, but not in GFS. For NTA, taxes on products and production are required to adjust consumption and labor income to their pre-tax values. Social contributions are also essentially identical in GFS and SNA. GFS and SNA use different sub-categories to classify taxes and social contributions. These sub-categories are useful for reclassifying taxes and social contributions by source for NTA public transfer outflows. The GFS classification system places more emphasis on the source of revenue in its classification system and, hence, the correspondence between the GFS and SNA classification systems are somewhat closer.

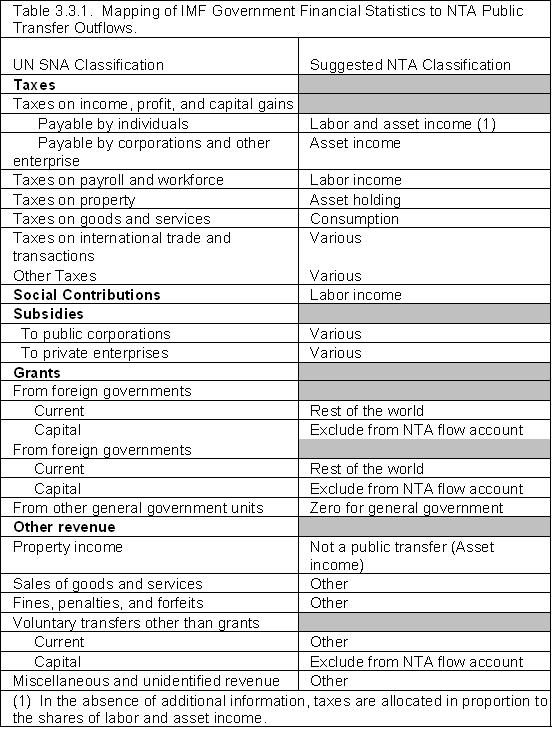

In Table 3.3.1. NTA public transfer outflows and their GFS counterparts are identified. The suggested NTA classification is suggestive rather than definitive. In some case, the classification will depend on more details on taxes than provided in the broad classification. For example, Taxes on international trade and transactions may include taxes on producers of exports (labor and asset income), consumers of imported goods (consumption), and/or consumers of exported goods (ROW). NTA public transfer outflows are reported as Revenue in GFSM 2001 (Table 5.1: Classification of Revenue, p 49) except for subsidies which are reported as Expenditure in GFSM 2001 (Table 6.1: Economic Classification of Expense, p 63).

Grants in GFS refer to transfers between governments and international organizations. Grants are further distinguished as current and capital transfers. The Flow Account in SNA includes only current transfers. As in SNA capital transfers are reported in a separate account (Asset Transfer Account in NTA and Capital Account in SNA). Thus, public revenues from capital transfer must not be included in public transfer outflows. The same principle applies to Voluntary transfers other than grants, capital. These must be excluded from the flow Account, and included in the Asset Transfer Account.

Public transfer inflows are reported in GFS as Expense classified in two ways: the economic classification of expense (GFSM 2001 Table 6.1) or by the function of government (GFSM 2001 Table 6.2). The cross-classification of Expense by function and economic classification (GFSM 2001 Table 6.3) is required to construct NTA from GFS. The classification of function in GFS follows the UN COFOG (Classification of Functions of Government) System as described above.

The economic classification in GFS can be used to separate in-kind transfers from cash transfers. Recall that in-kind transfers are equivalent to public consumption in NTA and, hence, the same values must be used for constructing the economic lifecycle and public transfers. In-kind transfers include compensation of employees (21), use of goods and services (22), consumption of fixed capital (23). In addition, in-kind social benefits are classified as in-kind transfers and public consumption in NTA. Cash transfers inflows consist of Grants (current only), Social benefits (in cash), and Miscellaneous other expense (current only).

Asset-based Reallocations

In NTA the age profile of asset income does not depend on its components. Hence, only total asset income is required to construct the accounts. Of course, researchers may be interested in the components of asset income as a means of understanding the public sector and its role in inter-age transfers. Asset income consists of the Operating surplus of general government and Property income in the SNA classification.

There is no GFS counterpart of Operating surplus. Property income sub-categories in GFS are essentially equivalent to those used in SNA. In NTA asset income is a net measure. For example, interest income is interest revenue less interest expense. Hence, net property income is equal to Property income less property expense as reported in GFS. Property expense in GFS is classified as Interest (item 24) plus Property expense other than interest (item 281) in Table 6.1: Economic Classification of Expense (p. 63).

Public saving in NTA is equivalent to the SNA concept. There is no exact counterpart in GFS, because saving does not include net capital transfers. Public saving can be calculated from GFS as the Net Operating Balance less Net Capital Transfers Receivable (Table 4.1 Statement of Government Operations, GFSM 2001).

-- Go to next page 4. Private Reallocations

-- Back to Table of Contents